60-day test period | ~10 min read

QUICK VERDICT

Wise: Our Verdict

Wise is not perfect but for the core use case it was built for; fair, transparent, affordable international transfers; it is the best widely available consumer product in the market. The bank exchange rate markup costs you $300 on a $10,000 transfer. Wise eliminates it entirely. For expats, remote workers, and frequent international senders, that single fact justifies the platform. The customer service limitation is real but invisible to the majority of users who never encounter a problem.

🔒 Opens on the marketplace. No extra cost to you. Read CritiqueHQ‘s full Affiliate Disclosure.

Wise: Pros & Cons

✅ PROS/ WHAT WE LOVED

⚠️CONS/ WHAT TO KNOW FIRST

Wise Review: What Is Wise and How Does It Actually Work?

Wise is a financial technology company, not a bank, which is a distinction worth understanding before you send money through it.

It was founded in London in 2011 by Kristo Käärmann and Taavet Hinrikus, two Estonian co-founders who were personally losing money to bank exchange rate markups every month. One was paid in British pounds and needed euros; the other received euros and needed pounds. They started exchanging money directly between themselves at the mid-market rate. Then they built a platform to let everyone do the same.

The core mechanism, called the peer-to-peer matching model in its early form, has since evolved into a more sophisticated local currency pooling system. The key outcome is the same: Wise uses the real mid-market exchange rate with no markup, charging a small, transparent percentage fee instead.

Here’s what that looks like in practice:

- You want to send £1,000 to a friend in the US

- Wise shows you the exact mid-market rate (the same one on Google)

- It charges a transparent fee (typically 0.4%–1.5%, depending on currency pair and method)

- Your recipient gets the full converted amount minus only that disclosed fee

No markup baked into the rate. No surprise deductions on arrival. No fine-print surcharges.

You may read the Financial Times article Lex in depth — remittance fintechs herald a payments revolution

This is the core value proposition. Everything else, the multi-currency account, the debit card, and the business tools, is built on top of this foundation.

Wise Review: The 9 Honest Truths About Using Wise in 2026

Truth 1: The Exchange Rate Advantage Is Real and Significant

Let’s put numbers on this.

The average UK high street bank charges a 3–5% markup on the exchange rate for international transfers. SWIFT-based wire transfers through US banks typically cost a $25–$45 flat fee plus a 1–3% rate markup.

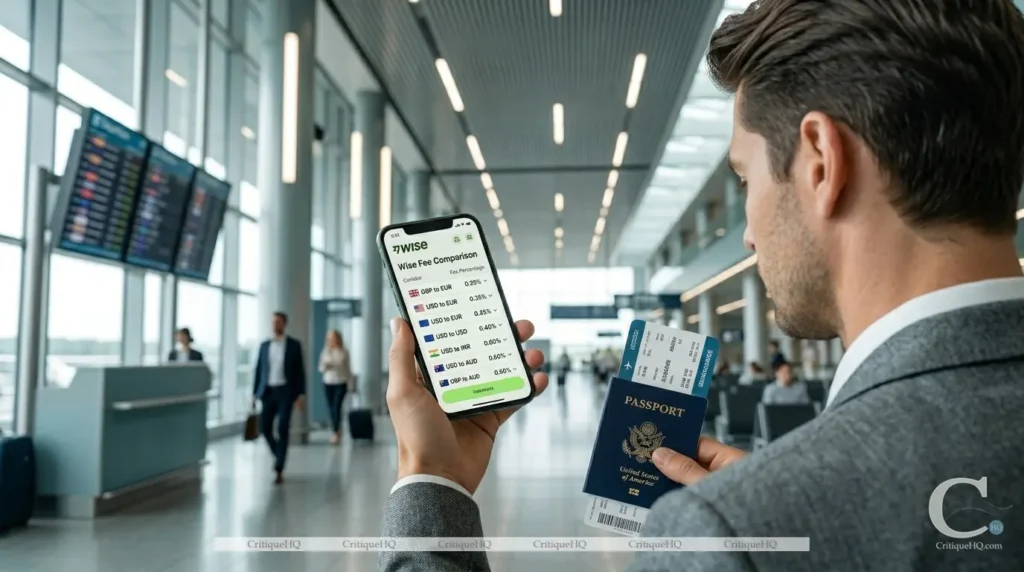

Wise charges a transparent fee of approximately:

- 0.4%–0.7% for major currency pairs (USD/EUR, GBP/USD, EUR/GBP)

- 0.7%–2% for less common pairs (SGD, HKD, INR, ZAR)

- Zero markup on the exchange rate itself

On a $5,000 transfer from USD to EUR:

- Traditional bank: $5,000 at a marked-up rate = ~$150–$200 lost to rate markup + $25–$45 wire fee

- Wise: $5,000 at mid-market rate, ~$25–$35 transparent fee total

That’s $140–$210 saved on a single transfer. For expats and remote workers sending money regularly, monthly, or even annually, the savings are significant.

You may check → World Bank: Remittance Prices Worldwide Database

The verdict: The rate advantage is not marketing copy. It’s measurable, consistent, and the primary reason Wise has 16+ million customers.

Truth 2: The Fees Are Transparent, But Not Always the Lowest

Wise markets itself on transparency, and it delivers on that. Every fee is shown before you confirm a transfer. No surprises on arrival.

But “transparent” and “lowest possible” are not always the same thing.

For very large transfers (over $50,000–$100,000), specialist currency brokers like OFX or TorFX sometimes offer better rates through negotiated pricing, particularly for regular high-volume senders. Wise doesn’t negotiate; its fee structure is algorithmic and standardized.

For small transfers (under $200), the minimum fee means the percentage effectively rises; a $50 transfer might carry a $2–3 fee, making Wise less competitive against certain bank-to-bank apps for tiny amounts.

The sweet spot for Wise’s fee structure: transfers between $500 and $50,000 in major currency pairs.

You may read this article on our site → 5 Best Budgeting Apps of 2026: Reviewed and Ranked for Real People

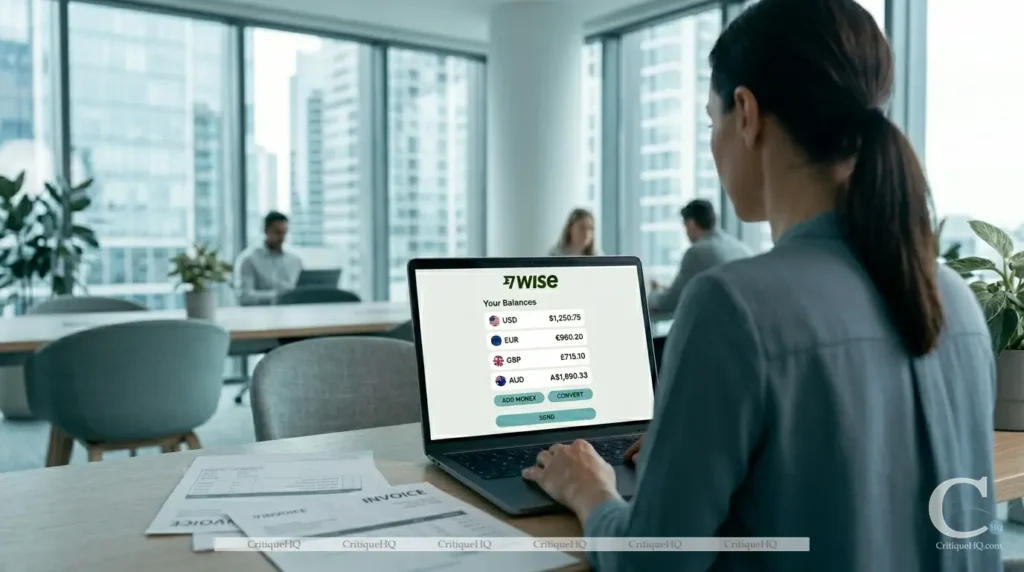

Truth 3: The Multi-Currency Account Is Genuinely Useful

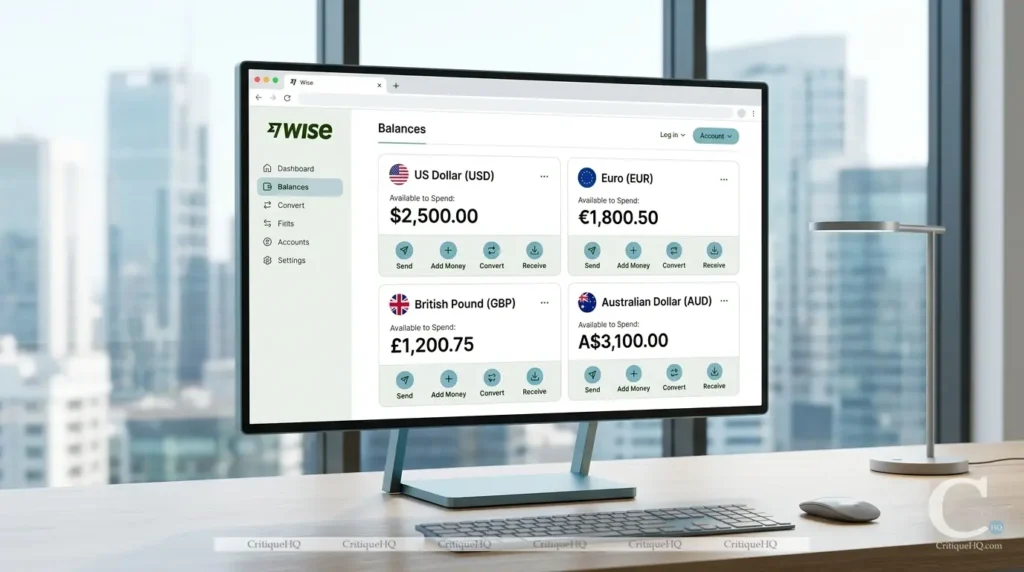

Beyond transfers, Wise offers a multi-currency account (called a Wise Account) that lets you hold, receive, and spend money in 40+ currencies simultaneously.

Here’s what that means practically:

- Local bank details in 9 currencies, you get real account numbers and sort codes in USD (US), EUR (EU), GBP (UK), AUD (AU), NZD (NZ), SGD (SG), CAD (CA), HUF (HU), and TRY (TR). This means you can receive international payments like a local, without triggering cross-border fees.

- Convert between currencies at mid-market rates within the account, useful for holding whichever currency is currently strongest before converting.

- Earn interest on balances (available in select currencies through Wise’s interest feature, rates vary and are variable).

For freelancers billing international clients, remote workers receiving salaries abroad, or expats managing finances across two countries, this is genuinely powerful. You can invoice a US client in USD, receive the payment to your Wise USD account, and convert it to GBP (or any other currency) at a moment of your choosing.

You may check the Wise of FCA → Register of Authorised Electronic Money Institutions: Wise Payments Limited

Free to open. No minimum balance. No monthly fee.

Check whether your specific currency corridor is supported before transferring.

Truth 4: Transfer Speed Is Usually Fast, But Not Guaranteed

Wise quotes transfer times that are typically accurate, but there’s important nuance.

Typical transfer times by method:

|

Transfer Type |

Typical Speed |

|---|---|

|

Card payment (debit/credit) |

Minutes to a few hours |

|

Bank transfer (major corridors) |

Same day or next business day |

|

Bank transfer (less common corridors) |

1–5 business days |

|

SWIFT-required transfers |

2–5 business days |

The marketing emphasizes speed, and for major corridors (USD→EUR, GBP→USD, EUR→AUD), Wise genuinely is fast, often with same-day delivery.

Where it slows down: Transfers to certain countries require SWIFT networks, which Wise uses as a fallback. SWIFT is slow by nature; 2–5 days is not unusual. This affects less-common corridors more than major ones.

Compliance holds: Like any regulated financial institution, Wise may hold transfers for verification. This most commonly affects first-time large transfers, sudden changes in transfer behavior, or certain destination countries. These holds are typically resolved within 24–48 hours, but they can feel alarming if you’re not expecting them.

Truth 5: The Wise Debit Card Is One of Its Best Features

The Wise debit card (available in most countries where Wise operates) extends the account’s utility significantly.

Key features:

- Spend in 150+ currencies at the mid-market rate with a small conversion fee (0.4%–1.5%)

- Free ATM withdrawals up to $100–$250/month (limits vary by region), then 1.75% + flat fee above the limit

- Works anywhere Visa or Mastercard is accepted

- Instant spending notifications and card freeze option via app

- Virtual card available immediately; physical card ships in 7–14 days

For travelers, the Wise card is one of the most cost-effective ways to spend abroad. For expats who regularly spend in their host country’s currency, it eliminates the need for a local bank account for day-to-day transactions.

The ATM caveat: The free withdrawal limit resets monthly. For heavy ATM users, the limit will be reached, plan accordingly or supplement with a local account.

Truth 6: Security Is Robust, But Wise Is Not a Bank

This matters and is worth being clear about.

Wise is not a bank. It is an Electronic Money Institution (EMI), regulated by the FCA in the UK, FinCEN in the US, and equivalent bodies in the 40+ countries where it operates.

As an EMI, Wise is required to safeguard your funds, meaning your money is held in regulated, ring-fenced accounts at major banks, separate from Wise’s operating capital. If Wise were to fail, your funds are protected through this safeguarding arrangement.

However, FSCS protection (UK) and FDIC insurance (US) do not apply to Wise balances, as they apply only to licensed banks. The safeguarding model offers meaningful protection, but it is not the same as deposit insurance.

You may check on the FCA website → Safeguarding Requirements for Electronic Money Institutions — Consumer Guidance

Practical implication: For the amounts most people transfer or temporarily hold in Wise (hundreds to low thousands), the risk is negligible in practice. For large, long-term balances, a regulated bank account is the more conservative choice.

On the fraud and security front: Wise uses 2FA, biometric login, real-time transaction notifications, instant card freeze, and advanced fraud detection. Its security track record is strong.

Truth 7: The Business Account Is a Separate, Powerful Offering

Wise Business deserves its own mention because it goes well beyond what a personal account offers.

Wise Business includes:

- Batch payments: pay up to 1,000 recipients in one upload (CSV format); transforms international payroll

- API access: Integrate Wise transfers directly into your financial stack or payment system

- Accounting integrations: Xero, QuickBooks, FreeAgent, and more; automatic sync reduces reconciliation time

- Team access controls: Add team members with role-based permissions; approve transfers without sharing account credentials

- Business debit cards: Issue cards per team member with individual limits

- Local account details: Receive international payments like a local business in 9 currencies

For small businesses, agencies, or freelancers managing international client payments and supplier payouts, Wise Business is a category-defining product.

The cost: Wise Business charges a one-time account opening fee in some regions (~$31 USD / £45 GBP). Transfer fees apply at the same rate as personal accounts.

Truth 8: Wise Has Specific Country and Use-Case Limitations

Wise is not available everywhere, and some users will hit limitations that matter.

Countries where Wise is not available for sending: Cuba, Iran, North Korea, Russia, and a small number of other sanctioned territories, as per the standard for any regulated financial institution.

Currency corridors where Wise has no direct route: Some currency pairs require conversion through an intermediate currency (e.g., sending to certain African and South Asian currencies). This adds a conversion step and slightly higher effective cost. Always check the specific corridor before assuming Wise covers it.

Cash payments: Wise is fully digital. No cash deposits, no cash withdrawals from Wise itself (only via debit card at ATMs). If part of your workflow involves physical cash, Wise doesn’t solve that.

Large transfers (100k+): As noted above, specialist currency brokers may offer more competitive rates at very high volumes. Wise’s flat algorithmic fee doesn’t scale down for large amounts the way negotiated broker rates can.

Truth 9: Customer Service Is the Weakest Part of the Experience

Every major Wise review surfaces the same complaint: customer service is inadequate for the scale of the product.

Wise’s primary support channel is in-app chat, supplemented by email. There is no phone support for standard personal accounts. Response times vary, quick for simple queries, potentially slow (48–72 hours) for complex issues or account verification holds.

For most day-to-day users who never encounter a problem, this is invisible. For users whose transfer is held for compliance review or whose account is flagged unexpectedly, the lack of phone support and variable chat response times can be deeply frustrating, particularly when time-sensitive transfers are involved.

The community forum and help documentation are genuinely good, extensive, well-organized, and often sufficient for resolving issues without contacting support.

Business accounts have a dedicated support queue with better response times. If your use case is high-volume, the business tier’s improved support access is worth factoring in.

How Wise Compares to the Alternatives

| Feature | ⭐ Wise Best Pick | Revolut | OFX | PayPal | Western Union |

Your Bank |

|---|---|---|---|---|---|---|

| Exchange Rate |

Mid-market; 0 markup |

Mid-market (weekly) |

Near mid- market |

3% to 4% markup |

High markup |

3% to 5% markup |

| Fee Structure |

0.4% to 2% transparent |

Free tier limited |

Negotiated (large amounts) |

1.99% to 3.99% |

Varies; often high |

$25 to $45 flat + markup |

| Multi-Currency Account |

Yes; 40+ currencies |

Yes; 30+ currencies |

No | No | No | Rarely |

| Local Bank Details |

Yes; 9 currencies |

Yes; select currencies |

No | No | No | No |

| Debit Card | Yes | Yes | No | Yes | No | Yes |

| Cash Pickup |

No | No | No | No | Yes | No |

| Best Transfer Size |

$500 to $50,000 |

Small daily spending |

$50,000+ | Under $500 |

Cash collections |

Any (at high cost) |

| Regulation | FCA; FinCEN; ASIC |

FCA; multiple |

ASIC; FinCEN |

FCA; FinCEN |

FinCEN | FDIC; varies |

| Best For | Core international transfers |

Daily multi-currency spending |

High- volume large transfers |

Consumer convenience |

Cash collection globally |

Existing relationship only |

Who Is Wise Actually Built For?

The platform is excellent, within its intended use cases. Let’s be specific.

✅ Wise is a strong fit if you:

⚠️Wise is a less ideal fit if you:

Wise Scoring Breakdown

|

Overall Score |

8.6/10 |

|

|---|---|---|

|

Exchange Rate Fairness |

10/10 |

|

|

Fee Transparency |

10/10 |

|

|

Multi-Currency Account |

9/10 |

|

|

Debit Card Usability |

9/10 |

|

|

Security and Regulation |

8/10 |

|

|

Transfer Speed (major corridors) |

8/10 |

|

|

Business Features |

9/10 |

|

|

Geographic Coverage |

8/10 |

|

|

Customer Service |

6/10 |

|

|

Transfer Speed (minor corridors) |

6/10 |

Bottom line: This Wise review lands on a clear conclusion: Wise is not perfect, but for the core use case it was built for, fair, transparent, affordable international transfers, it is the best widely available consumer product in the market.

The bank exchange rate markup is a $300 tax on a $10,000 transfer. Wise eliminates it. For anyone moving money internationally with any frequency, that alone justifies trying it.

The customer service limitation is real and worth acknowledging. But for the vast majority of users who never encounter a problem, it’s invisible, and the experience of using Wise itself is clean, intuitive, and genuinely trustworthy.

You may read this review on our site → eToro vs Coinbase 2026: Which Platform Should You Actually Use?

Frequently Asked Questions

Ready to Stop Losing Money on Exchange Rates?

Opening a Wise account is free and takes under 5 minutes. The mid-market rate with no markup applies from your very first transfer. For expats, remote workers, and frequent senders, the savings over a year are significant.

🔒 Opens on the marketplace. No extra cost to you. Read CritiqueHQ‘s full Affiliate Disclosure.

Related Posts

eToro vs Coinbase 2026: Which Platform Should You Actually Use?

Here’s the situation. You’re ready to buy crypto or stock, or both. You’ve narrowed it down to two of the…

Wise Review 2026: The Honest Truth About International Money Transfers

60-day test period | ~10 min read QUICK VERDICT Wise: Our Verdict Wise is not perfect but for the core…

5 Best Budgeting Apps of 2026: Reviewed and Ranked for Real People

Most people don’t have a spending problem. They have a visibility problem. You’re not broke because you’re irresponsible – you’re…

[…] You may read in our review, Wise Review 2026: The Honest Truth About International Money Transfers. […]

[…] You may check our Wise review here: Wise Review 2026: The Honest Truth About International Money Transfers […]