🔒 Opens on marketplace. No extra cost to you. Read CritiqueHQ‘s full Affiliate Disclosure.

Most people don’t have a spending problem. They have a visibility problem.

You’re not broke because you’re irresponsible – you’re broke because money moves silently. It leaves your account in $12 increments and $47 charges, and one impulsive online cart you told yourself was a “treat,” and by the 20th of the month, you’re doing mental math that doesn’t add up.

That’s where the best budgeting apps of 2026 come in. Not to judge you. Not to put you on a financial starvation diet. But to give you a clear picture of where your money is actually going, so you can make real decisions, not guesses.

We tested and reviewed the top options on the market. Here’s what we found.

What Makes a Budgeting App Actually Worth Using in 2026?

Before we get to the list, let’s talk about what separates a great budgeting app from one that gets deleted after three weeks.

Most people abandon budgeting apps for one of three reasons:

- Too much manual work – if you have to hand-enter every transaction, you won’t.

- Too rigid – zero-based budgeting is powerful but alienating if you’re a beginner.

- No clear payoff – if the app doesn’t show you something meaningful within the first session, the motivation evaporates.

The apps on this list were evaluated on five criteria:

- Ease of setup – how long does it take to connect your accounts and see something useful?

- Automation – does it pull transactions, categorize them, and flag anomalies without your help?

- Budgeting methodology – does it fit the way real people actually spend money?

- Financial insight quality – does it just track, or does it teach?

- Value for money – does the free tier offer enough, or is the paywall justified?

You may check our Wise review here: Wise Review 2026: The Honest Truth About International Money Transfers

The 5 Best Budgeting Apps 2026: Reviewed and Ranked

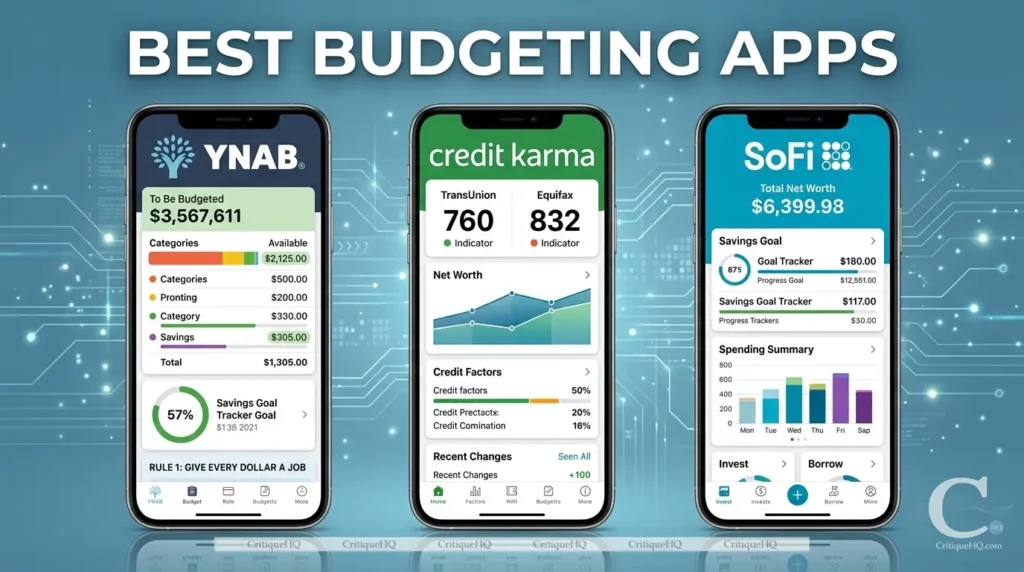

#1. YNAB (You Need a Budget): Best for Getting Serious About Money

Best for: People ready to change their relationship with money – not just track it.

YNAB is not the easiest app on this list. It’s the most transformative.

The philosophy behind YNAB is called zero-based budgeting: every dollar you earn gets a job before you spend it. You don’t budget based on projected income; you budget based on money you actually have, right now, in your accounts.

It sounds simple. It is, once you internalize it. But getting there takes about two weeks of consistent use, which is why YNAB has the most passionate (bordering on evangelical) user base of any budgeting app in existence.

The results people report are not modest. YNAB’s own data shows new users save an average of $600 in their first two months and over $6,000 in their first year. Independent surveys of long-term users echo similar numbers.

What YNAB Does Well:

- The Four Rules – YNAB’s budgeting framework is genuinely well-designed and grounded in behavioral economics. It teaches you to age your money (spend this month on last month’s income), which is one of the most effective financial stability tactics available.

- Real-time sync – connects to most major banks and syncs transactions automatically.

- Goal tracking – set specific targets (emergency fund, vacation, debt payoff) and YNAB shows you exactly how your current budget either supports or undermines those goals.

- Reports – net worth tracking, spending trends, and income vs. expense visualizations that are genuinely illuminating, not just pretty graphs.

- Multi-device – desktop web app plus iOS and Android, all synced.

The Honest Downsides:

- It costs money – $14.99/month or $99/year. No meaningful free tier beyond the 34-day trial.

- The learning curve is real – expect 2–3 weeks before it clicks. Many people quit during this window and miss the breakthrough.

- Bank connectivity can glitch – like all apps that sync to financial institutions, YNAB occasionally loses connection to accounts. Manual re-linking is occasionally required.

Who Should Skip It: If you want something you can set up in 10 minutes and forget about, YNAB will frustrate you. It’s for people who are ready to engage with their finances actively, at least weekly.

Who Should Sign Up Today: Anyone who has said “I don’t know where my money goes” more than twice. Anyone building toward a specific financial goal. Anyone in debt who wants a system, not just a spreadsheet.

#2. Credit Karma: Best Free All-in-One Financial Dashboard

Best for: Beginners, passive trackers, and anyone who wants a free, low-maintenance financial overview.

Credit Karma started as a credit score tracker. In 2026, it has evolved into something significantly more ambitious, a full personal finance dashboard that competes meaningfully with paid alternatives.

And it is completely free. Always has been. The model is advertising-based: Credit Karma earns money by recommending financial products (credit cards, loans, insurance) tailored to your profile. You get the tools for free; they get to show you offers. It’s a trade-off worth understanding before you sign up.

What Credit Karma Does Well:

- Free credit monitoring – weekly updated TransUnion and Equifax scores with explanations of what’s affecting them. This alone is worth the signup.

- Net worth tracking – connect bank accounts, investment accounts, and loans to see your actual financial picture in one place.

- Spending overview – automatic transaction categorization and monthly spending summaries. Not as granular as YNAB, but solid for passive monitoring.

- Credit card and loan recommendations – genuinely personalized based on your actual credit profile, not generic suggestions.

- Tax filing integration – Credit Karma Tax (now Cash App Taxes after the Square acquisition) is free and solid for straightforward returns.

- Savings account – Credit Karma Money Save offers a competitive APY with no minimums.

The Honest Downsides:

- Budgeting depth is limited – Credit Karma is excellent for awareness and monitoring, but it doesn’t have YNAB’s budgeting methodology or goal-setting depth.

- It’s ad-supported – you will see financial product recommendations throughout the app. If that feels intrusive, it can undermine the experience.

- Transaction categorization isn’t perfect – it occasionally misfires (a restaurant charged as “shopping,” for example), and corrections are manual.

Who Should Use Credit Karma: Anyone who wants a free, zero-effort financial dashboard. It’s the best starting point for someone who has never tracked their spending or credit before. It’s also an excellent complement to a more active tool like YNAB – use Credit Karma for the macro view, YNAB for the detailed budget management.

#3. SoFi: Best for Building Wealth While You Budget

Best for: Young professionals who want banking, investing, and budgeting under one roof.

SoFi is not a pure budgeting app. It’s a full-service fintech platform, and that’s precisely what makes it powerful for a specific type of user.

The budgeting and spending insights tools inside SoFi are genuinely good. But the reason SoFi earns a spot on this list is its integration: your budget, your high-yield savings, your investment account, and your loan management all live in the same ecosystem. For people who want to consolidate their financial life, that’s a significant advantage.

What SoFi Does Well:

- High-Yield Savings Account – SoFi’s HYSA consistently offers one of the more competitive APYs in the online banking space. Budgeting toward a savings goal in an app that also holds your savings account is genuinely useful.

- Spending insights – automatic transaction categorization, monthly summaries, and category breakdowns that are clean and readable.

- Invest integration – SoFi Invest lets you open a brokerage account, IRA, or automated (robo-advisor) investing account directly within the app.

- Loan management – student loan refinancing, personal loans, and home loans — with a dashboard that shows all your debt obligations alongside your budget.

- No account fees – SoFi Checking and Savings accounts have no monthly fees and no minimum balances.

- Credit score monitoring – a weekly updated score is included free with any account.

You may check the FDIC’s SoFi Bank, National Association

The Honest Downsides:

- Budgeting tools are not as deep as dedicated apps – SoFi doesn’t have YNAB’s methodology or granular category controls. If your primary need is detailed budget management, SoFi is not the right tool.

- Full value requires using SoFi’s financial products – the integration is powerful only if you actually move your banking and investing into SoFi. If you just want the insights, it’s underwhelming.

- Customer service has been a friction point – some users report delays in support resolution, a common fintech growing pain.

Who Should Use SoFi: Young professionals who want to simplify their financial stack. If you’re currently managing a checking account at one bank, savings at another, investments on a third platform, and student loans through a servicer – SoFi’s consolidation proposition is genuinely compelling.

#4. Monarch Money: Best YNAB Alternative for Couples and Families

Best for: Couples managing joint finances, families with complex budgets, and YNAB refugees who want more flexibility.

Monarch Money launched in 2021 and has grown rapidly – partly because it filled the gap left by Mint’s shutdown in 2024, and partly because it’s genuinely excellent.

The interface is the cleanest and most modern of any app on this list. The financial dashboards are beautiful without being style over substance. And the collaborative features, where two people can both see and edit the same budget in real time, are significantly better than any competitor.

What Monarch Money Does Well:

- Joint budgeting – built for multiple users from the ground up. Both partners can view, edit, and comment on the budget simultaneously. This is YNAB’s weakest area by comparison.

- Flexible budgeting methodology – supports zero-based, category-based, and hybrid approaches. You’re not forced into a single system.

- Investment tracking – portfolio performance, asset allocation, and net worth tracking are more detailed than Credit Karma and on par with Personal Capital (now Empower).

- Custom reports – build your own spending reports by date range, category, merchant, or account. Excellent for people who like to dig into the data.

- Recurring transaction management – Monarch automatically identifies and tracks recurring charges, subscriptions, and bills. One of the best implementations of this feature in the category.

The Honest Downsides:

- Costs money – $14.99/month or $99.99/year. Similar price point to YNAB, which raises the question of which methodology suits you better.

- Smaller ecosystem than SoFi – no banking, investing, or lending integration. It’s a pure budgeting and tracking tool.

- Relatively new – fewer third-party reviews and long-term user data than YNAB or Credit Karma.

Who Should Use Monarch: Couples who fight about money (or want to proactively not fight about money). Families with multiple income streams and complex category structures. Former Mint users looking for the closest modern equivalent, and then some.

You may read the Consumer Financial Protection Bureau’s Budgeting: How to create a budget and stick with it.

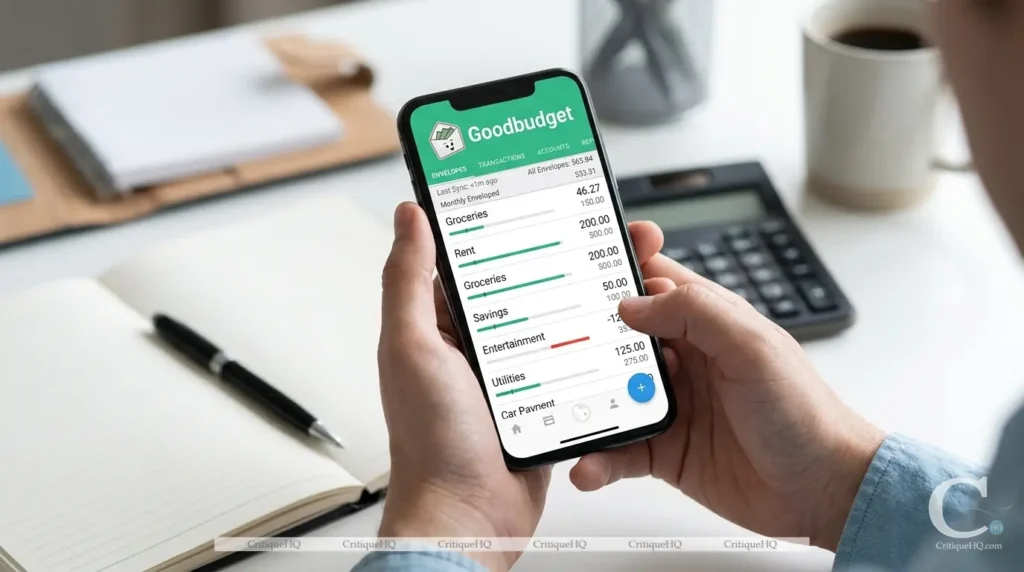

#5. Goodbudget: Best for Cash-Envelope Budgeting Without the Actual Cash

Best for: Envelope budgeting believers, cash-flow disciplinarians, and anyone who’s read Dave Ramsey.

The envelope budgeting method is old. Older than apps, older than credit cards, older than most financial advice on the internet. You divide your cash into physical envelopes, one for groceries, one for rent, one for fun, and when the envelope is empty, you stop spending.

It works. Behavioral economists have studied it extensively. Physical constraint, even simulated constraint, reduces impulsive spending better than abstract budget awareness.

Goodbudget digitizes the envelope method without requiring physical cash. You create digital “envelopes,” fund them at the start of each month or paycheck, and track spending against each one. When an envelope hits zero, you’re done, or you consciously move money from another envelope.

What Goodbudget Does Well:

- The method itself – envelope budgeting is one of the most proven behavioral finance tools available. Goodbudget is the best digital implementation of it.

- Shared envelopes – you and a partner can both spend from the same digital envelopes in real time, with instant syncing.

- Simplicity – the interface is intentionally simple. There’s no net worth tracking, no investment integration, no noise. Just your envelopes and your spending.

- Free tier – 20 envelopes and 1 account on the free plan, which is workable for most individuals.

The Honest Downsides:

- No automatic bank sync on the free tier – you enter transactions manually on the free plan. The $10/month Plus plan adds bank sync.

- No investment or net worth tracking – Goodbudget does one thing. If you want the broader financial picture, you’ll need a second app.

- Interface looks dated – not as polished as Monarch or SoFi. This bothers some users more than others.

Who Should Use Goodbudget: Anyone whose spending problem is specifically about in-the-moment impulse control. The envelope method works best when the psychological constraint of a “depleting envelope” changes behavior, and for people wired that way, Goodbudget is transformative.

Head-to-Head: The Best Budgeting Apps 2026 at a Glance

|

App |

Free? |

Auto-Sync |

Budgeting Depth |

Best Feature |

Best For |

|---|---|---|---|---|---|

|

YNAB |

Trial only |

✅ |

⭐⭐⭐⭐⭐ |

Zero-based methodology |

Serious budgeters |

|

Credit Karma |

✅ Always |

✅ |

⭐⭐⭐ |

Free credit + spending overview |

Beginners, passive trackers |

|

SoFi |

✅ Always |

✅ |

⭐⭐⭐ |

All-in-one financial platform |

Young professionals |

|

Monarch Money |

Trial only |

✅ |

⭐⭐⭐⭐⭐ |

Couples & joint budgeting |

Couples, families |

|

Goodbudget |

✅ (limited) |

Plus plan |

⭐⭐⭐⭐ |

Envelope method |

Cash-flow disciplinarians |

You may read the NIH’s “Impact of financial literacy, mental budgeting, and self-control on financial well-being.”

How to Choose the Right Budgeting App for Your Situation

The best budgeting app is the one you’ll actually use. That sounds obvious, but it isn’t.

Here’s a quick decision tree:

“I’ve never tracked my spending, and I want to start with zero friction.” → Start with Credit Karma (free, automatic, no learning curve).

“I want to seriously change my financial behavior, and I’m willing to invest time.” → YNAB is the answer. Commit to the 34-day trial.

“My partner and I need to manage money together without fighting about it.” → Monarch Money was built for this exact situation.

“I want to bank, save, invest, and budget in one place.” → SoFi – consolidate your financial stack.

“I overspend impulsively and need hard guardrails.” → Goodbudget – the digital envelope method addresses impulse spending directly.

You may check our eToro vs Coinbase comparison article here: eToro vs Coinbase 2026: Which Platform Should You Actually Use?

Frequently Asked Questions

What is the best free budgeting app in 2026?

Credit Karma is the best fully free option; it includes credit monitoring, spending tracking, net worth, and savings account features at no cost. For envelope budgeting, Goodbudget’s free tier (20 envelopes) is also solid.

Is YNAB worth the subscription cost?

For most active users: yes. YNAB costs about $99/year. If it helps you save even $600 in your first two months (the average reported by new users), the ROI is clear. The 34-day free trial is long enough to know whether it will work for you.

Are budgeting apps safe to link to your bank account?

The apps on this list use bank-level 256-bit encryption and connect via read-only API (they can see your transactions but cannot move money). They also use third-party services like Plaid for the connection layer.

That said, no digital service is risk-free. Use strong, unique passwords and enable two-factor authentication on any financial app.

What happened to Mint? What should Mint users switch to?

Mint shut down in January 2024. Monarch Money is the closest equivalent in terms of features and interface. Credit Karma is the best free alternative. YNAB is the upgrade if you’re ready to get serious.

Can I use more than one budgeting app at the same time?

Absolutely, and many people do. A common combination: Credit Karma for passive credit and spending monitoring, plus YNAB or Monarch for active budget management.

The Bottom Line

The search for the best budgeting apps 2026 comes down to one question: what’s your actual problem?

If it’s visibility – you don’t know where your money goes – start with Credit Karma.

If it’s behavior — you know where it goes and you can’t stop – try YNAB or Goodbudget.

If it’s coordination – you and a partner can’t get on the same page — Monarch Money.

If it’s consolidation, too many financial accounts, not enough clarity – SoFi.

The apps exist. The tools are better than they’ve ever been. The only variable left is whether you are actually opening one.

Related Posts

eToro vs Coinbase 2026: Which Platform Should You Actually Use?

Here’s the situation. You’re ready to buy crypto or stock, or both. You’ve narrowed it down to two of the…

Wise Review 2026: The Honest Truth About International Money Transfers

60-day test period | ~10 min read QUICK VERDICT Wise: Our Verdict Wise is not perfect but for the core…

5 Best Budgeting Apps of 2026: Reviewed and Ranked for Real People

Most people don’t have a spending problem. They have a visibility problem. You’re not broke because you’re irresponsible – you’re…

🔒 Opens on marketplace. No extra cost to you. Read CritiqueHQ‘s full Affiliate Disclosure.

[…] You may read this article on our site → 5 Best Budgeting Apps of 2026: Reviewed and Ranked for Real People […]

[…] You may read our review, 5 Best Budgeting Apps of 2026: Reviewed and Ranked for Real People. […]